Fintech PM Trends: The Future of Financial Innovation: Here is a direct, actionable answer based on real interview data and hiring patterns from top tech companies.

Fintech product management is being reshaped by embedded finance, real‑time payments, and stricter regulatory oversight. PMs who combine deep domain knowledge with data‑driven experimentation will capture the most value. Preparing for these shifts requires a focus on concrete skills, not just generic product frameworks.

This article targets experienced product managers who are either already working in financial services or planning to move into a fintech role at a startup, scale‑up, or incumbent bank. It assumes familiarity with core PM practices such as roadmap prioritization and metrics definition, and it speaks to those who need to understand where the industry is heading and how to align their skill set accordingly.

What are the biggest fintech trends shaping product management in 2025?

The three trends that dominate roadmap conversations are embedded finance, real‑time settlement, and AI‑driven risk modeling. Embedded finance allows non‑financial platforms to offer banking‑like services through APIs, which shifts the PM’s focus from building standalone products to designing seamless integration layers.

Real‑time settlement, driven by instant payment rails such as FedNow and SEPA Instant, compresses settlement windows from days to seconds, forcing PMs to rethink liquidity management and fraud detection workflows. AI‑driven risk modeling is moving from retrospective scoring to continuous, behavior‑based underwriting, which requires PMs to collaborate closely with data scientists and to define clear model‑governance checkpoints.

In a Q3 debrief at a Series C lending platform, the hiring manager pushed back on a candidate who emphasized “building a new credit‑scoring engine” without showing how the model would be monitored for drift or how explainability would be delivered to regulators. The insight that emerged was that fintech PMs must treat model governance as a first‑class product requirement, not an afterthought. This reflects a broader organizational psychology principle: when technical depth is perceived as a risk mitigator, stakeholders grant PMs greater autonomy over experimentation.

The counter‑intuitive observation is that the most successful fintech PMs spend less time on feature ideation and more time on designing feedback loops that capture regulatory signals early. Not your ability to sketch a UI, but your capacity to embed compliance checkpoints into the development cycle determines how fast you can ship.

> 📖 Related: Applied Materials PMM hiring process and what to expect 2026

How do embedded finance and banking‑as‑a‑service affect PM roadmaps?

Embedded finance turns the PM into an orchestrator of third‑party capabilities rather than a builder of monolithic systems. Roadmaps now prioritize API reliability, developer experience, and compliance‑by‑design over traditional feature buckets. A typical roadmap might allocate 40 % of effort to API versioning and sandbox testing, 30 % to partner onboarding flows, and the remaining 30 % to analytics that measure uptake across partner channels.

During a hiring committee debate at a mid‑size BaaS provider, a senior PM argued that the team should invest in a low‑code integration studio to reduce partner ramp‑up time from six weeks to two days. The opposing view, backed by data from a recent partner survey, highlighted that partners valued security certifications more than speed. The committee concluded that the PM’s proposal ignored a key trust signal, illustrating the framework of “value‑vs‑risk trade‑off” that is unique to fintech ecosystems.

Not your roadmap’s feature count, but the clarity of your API contract’s service‑level objectives determines partner satisfaction.

Which regulatory changes are most relevant for fintech product managers?

Three regulatory shifts are reshaping product decisions: the expansion of open‑banking mandates in the U.S. and EU, the tightening of stable‑coin oversight under the forthcoming MiCA framework, and the heightened scrutiny of AI‑based credit models under the EU AI Act. Open‑banking requires PMs to design consent‑management flows that are both user‑friendly and auditable. Stable‑coin regulations demand transparent reserve reporting and redemption mechanisms, which affect product timing and go‑to‑market strategies. The AI Act introduces conformity‑assessment requirements for high‑risk scoring models, meaning PMs must allocate time for third‑party audits and documentation.

In a recent HC discussion at a payments startup, the compliance lead warned that a proposed “instant‑cash‑out” feature would violate the new liquidity‑coverage ratio rules unless the team could prove real‑time collateralization. The PM responded by proposing a dual‑track approach: a limited‑beta for low‑value transactions and a separate liquidity‑reserve pool for higher amounts. The insight was that regulatory constraints can become a source of differentiation when treated as design parameters rather than blockers.

Not your product’s novelty, but its ability to demonstrate ongoing compliance to regulators and auditors determines whether it reaches market.

> 📖 Related: cornell-to-google-pm-2026

How should I prioritize skills when transitioning into a fintech PM role?

Prioritize three skill clusters: financial‑domain fluency, data‑analytics proficiency, and stakeholder‑translation ability. Financial‑domain fluency means understanding core concepts such as net interest margin, capital adequacy, and settlement risk — not just being able to define them in an interview but being able to explain how they affect product economics.

Data‑analytics proficiency extends beyond SQL to include the ability to design experiments that isolate causal effects in low‑volume, high‑value transactions (e.g., using Bayesian uplift models for loan‑approval experiments). Stakeholder‑translation ability is the capacity to bridge the language gap between engineers, risk officers, and compliance lawyers, often by creating one‑page risk‑benefit summaries that satisfy both technical and governance reviews.

A concrete example comes from a product sense interview at a digital‑wallet firm where the candidate was asked to improve the success rate of cross‑border transfers. The strongest answer outlined a hypothesis‑driven experiment: vary the FX‑rate lock‑in window, measure impact on conversion and settlement failure, and then present a risk‑adjusted ROI calculation to the treasury team. The weaker answer listed UI improvements without linking them to financial outcomes. The hiring manager later noted that the candidate’s ability to tie a product change to a treasury KPI was the decisive factor.

Not your familiarity with agile ceremonies, but your capacity to speak the language of risk and return determines how quickly you gain credibility in fintech.

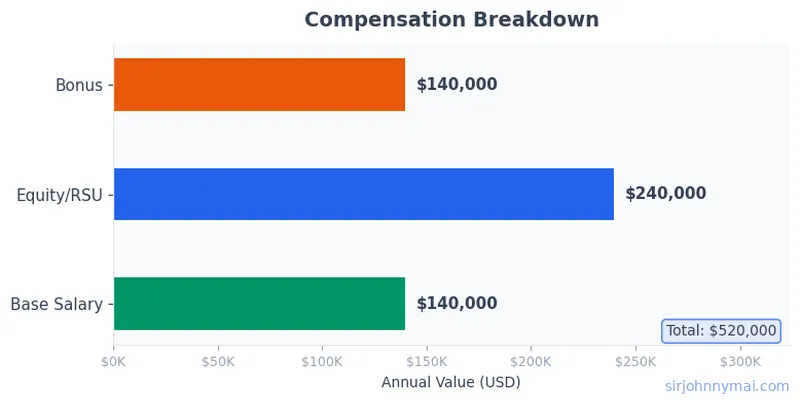

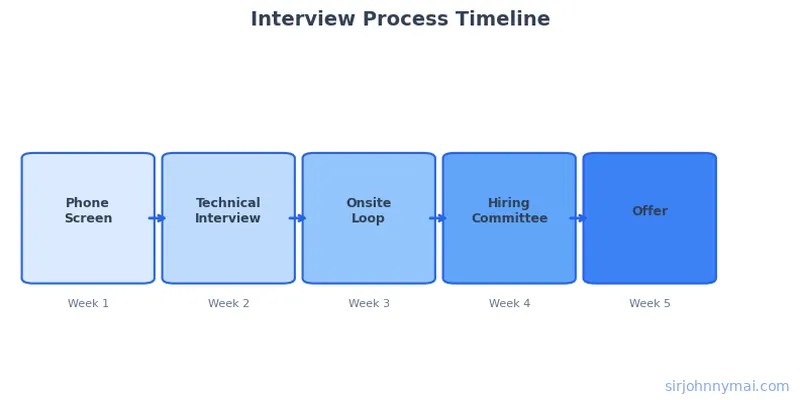

What compensation ranges and interview processes look like for fintech PMs at mid‑size and large firms?

Base salary for a fintech PM at a Series B‑C company typically falls between $140,000 and $190,000, with total compensation (including equity and bonus) reaching $240,000 to $300,000 at the 75th percentile. At larger incumbents or publicly traded fintechs, base ranges shift to $165,000–$220,000, with total packages often exceeding $350,000 when RSUs are factored in. Equity grants usually follow a four‑year vesting schedule with a one‑year cliff, and annual refreshes are common after the first 18 months.

Interview loops generally consist of four rounds: a product‑sense case (often a market‑sizing or go‑to‑market scenario), an execution deep‑dive (focusing on metrics definition and trade‑off analysis), a behavioral interview (testing leadership and conflict‑resolution), and a domain‑specific case (such as designing a compliant lending product or evaluating a stable‑coin mechanism). Take‑home assignments, when used, usually have a five‑day deadline and require a written product brief plus a rough mock‑up.

In a recent debrief at a global bank’s innovation lab, the hiring manager observed that candidates who treated the domain case as a pure product exercise — ignoring capital‑allocation constraints — scored lower on the execution round, even if their product ideas were creative. The insight was that fintech interviews weigh domain rigor as heavily as product creativity.

Not the number of rounds you survive, but how well you integrate financial constraints into your product thinking determines your offer outcome.

What to Focus On Before the Interview

- Review recent earnings calls and regulatory filings from three fintech firms you admire to identify recurring themes in their product strategy.

- Build a personal “finance‑for‑PMs” cheat sheet covering key ratios (ROE, CET1, LCR), payment‑rail characteristics, and basic API security standards (OAuth 2.0, mTLS).

- Practice translating a technical constraint (e.g., latency limits on real‑time settlement) into a product requirement and success metric.

- Run a mock product‑sense case that includes a regulatory angle — such as designing a new buy‑now‑pay‑later feature under upcoming BNPL disclosure rules.

- Work through a structured preparation system (the PM Interview Playbook covers embedded‑finance case studies with real debrief examples).

- Prepare two STAR stories that highlight your experience working with risk or compliance teams to ship a product.

- Set up a weekly habit of reading one analyst report on fintech market trends and noting one actionable insight for your own roadmap.

The Gaps That Kill Strong Applications

BAD: Focusing your interview prep solely on generic product frameworks like CIRCLES or SWOT without tying them to fintech‑specific constraints.

GOOD: In each practice case, explicitly state how capital‑adequacy, liquidity, or regulatory reporting limits shape your solution and how you would measure compliance impact.

BAD: Treating equity compensation as an afterthought and negotiating only base salary.

GOOD: Research the company’s most recent 409A valuation, understand the vesting schedule, and ask about refresh‑grant timing and performance‑based equity components during the offer conversation.

BAD: Assuming that a strong UI prototype will win a fintech product‑sense interview.

GOOD: Show how the UI change influences a key financial metric (e.g., reduces failed settlement rates by X % or improves net interest margin by Y basis points) and back it up with a simple calculation or data assumption.

FAQ

What is the most important metric for a fintech PM to track?

The most important metric depends on the product type, but a universally useful north‑star is risk‑adjusted return on capital (RAROC). It captures both the revenue generated by a feature and the capital or loss exposure it creates, allowing PMs to compare initiatives across lending, payments, and wealth‑management lines on a common basis.

How long does it typically take to move from a traditional tech PM role into a fintech PM role?

Transition timelines vary, but a realistic window is six to twelve months when you actively build domain knowledge, complete at least two fintech‑focused product projects (internal or side‑project), and tailor your resume to highlight financial‑services impact. Companies often look for evidence of recent fintech exposure rather than a sudden switch.

Should I learn to code to be effective as a fintech PM?

You do not need to become a software engineer, but proficiency in reading and writing SQL, understanding basic API contracts, and being able to prototype data pipelines in Python or R significantly improves your credibility with engineering and data‑science teams. The goal is to speak the same language as your technical partners, not to replace them.

Ready to build a real interview prep system?

Get the full PM Interview Prep System →

The book is also available on Amazon Kindle.