Fintech PM career growth follows a predictable trajectory if you understand the signal hierarchy: domain depth > product sense > leadership visibility. The opportunity set is expanding—fintech hiring grew 23% year-over-year in 2024—but the competition is fiercer because every PM from adjacent industries wants in. The real challenge isn't landing your first fintech PM role; it's surviving the first 18 months when you'll be expected to own P&L while still learning regulatory frameworks that most engineers never had to master.

Fintech PM career growth follows a predictable trajectory if you understand the signal hierarchy: domain depth > product sense > leadership visibility. The opportunity set is expanding—fintech hiring grew 23% year-over-year in 2024—but the competition is fiercer because every PM from adjacent industries wants in. The real challenge isn't landing your first fintech PM role; it's surviving the first 18 months when you'll be expected to own P&L while still learning regulatory frameworks that most engineers never had to master.

This is for product managers with 2-7 years of experience who are either trying to break into fintech from adjacent industries—e-commerce, SaaS, payments—or already in fintech and wondering why their career progression feels slower than peers at Stripe or Block. If you're asking "is fintech PM worth it" or "what do fintech companies actually want," read this.

What Fintech Companies Actually Want in Product Managers

Fintech companies want operators, not strategists. That's the fundamental miscalibration most candidates make.

In a 2023 debrief for a senior PM role at a Series C payments company, the hiring manager rejected a candidate from a top-tier strategy consultancy with this framing: "Her framework for merchant retention was beautiful. But she couldn't tell me what she'd do on Monday if we discovered our fraud rate spiked 2% overnight." The candidate had spent two years advising fintech clients but zero days shipping product under regulatory pressure.

What fintech companies signal for: PMs who have owned metrics that directly impact the company's survival—chargeback rates, approval rates, unit economics per transaction, compliance incident frequency. Not because these are more important than user retention or NPS, but because fintech operates in a zero-failure environment. One regulatory violation can end a company. One fraud breach can destroy trust that took years to build.

The contrast isn't strategy vs. execution. It's context-specific judgment. A PM from a consumer social app might have excellent experimentation skills. But can they make a call on a new lending product feature knowing that the legal team needs 6 weeks to review and the compliance deadline is in 4? That's the decision-making fintech interviewers are testing.

> 📖 Related: atlassian-pm-career-path-levels-2026

How Much Do Fintech PMs Actually Make

Compensation in fintech follows a bimodal distribution that catches candidates off guard.

At Series A and B fintechs, total compensation for a mid-level PM (3-5 years experience) typically ranges from $180,000 to $280,000, with equity that may be worth something in 4 years or nothing. At Series C and beyond—companies like Ramp, Brex, Stripe, Block—total compensation for the same level ranges from $280,000 to $400,000, with meaningful equity.

But here's what candidates don't negotiate: variable components and equity vesting cliffs.

In a 2024 offer negotiation I observed, a PM received a base salary of $220,000 from a late-stage fintech with an advertised TC of $320,000. The additional $100,000 was tied to company-wide revenue targets and a 4-year equity vest with a 1-year cliff. The candidate accepted without negotiating the component structure and lost roughly $80,000 in realized compensation when the company missed its revenue targets in year two.

Not salary, but structure. That's what determines your actual fintech compensation.

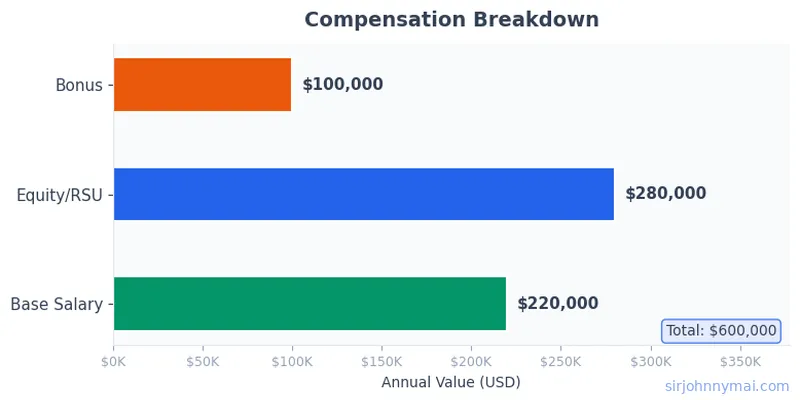

Senior PMs (6-9 years) at category leaders can reach $450,000 to $600,000 in total compensation. Director-level pushes toward $700,000+. But compensation at these levels comes with operational ownership that most PMs haven't experienced: managing P&L for a $50M+ revenue line, leading cross-functional teams of 15+, and presenting board-level updates quarterly.

What's the Career Path for a PM in Fintech

The typical fintech PM career path isn't a straight line. It's a fork.

After 3-5 years as a PM, you choose between two tracks that diverge sharply: product leadership (Principal PM, Group PM, VP Product) or domain specialization (Risk PM, Compliance PM, Growth PM). The mistake is assuming these tracks are interchangeable. They're not.

I watched a strong PM at a lending fintech get passed over for a Director role because she'd optimized for breadth—shipping products across consumer, SMB, and enterprise segments—while a peer with half her tenure got the promotion for going deep on the fraud domain. The hiring manager's reasoning: "We need someone who can walk into a regulatory meeting and speak the language fluently. That's not something you can fake with generalist experience."

The fintech career path rewards depth at the senior levels. Not because generalist skills don't matter, but because the regulatory and competitive complexity at scale requires someone who has seen the same edge cases multiple times.

Here's the realistic timeline: 2-4 years to go from PM I to PM II (or equivalent), 4-7 years to Senior PM, 7-10 years to Staff or Principal PM, 10+ years to Director. These timelines compress at high-growth companies (Brex promoted a PM to Director in 4 years) and extend at risk-averse incumbents (traditional banks may take 8+ years for the same progression).

The fork matters because your first 3 years in fintech determine which door stays open.

> 📖 Related: Microsoft PM vs Data Scientist career switch 2026

How to Break Into Fintech From Another Industry

Breaking in isn't about learning fintech. It's about translating your existing experience into fintech-native language.

The most common failure mode: candidates who spend months studying blockchain, DeFi protocols, and payment infrastructure without addressing the actual hiring signal. In a hiring committee I participated in, a candidate from a logistics SaaS company spent 20 minutes of a 45-minute interview explaining how supply chain payments worked. She never connected it to the actual role—building B2B expense management software.

The successful pattern is different. A PM from a food delivery company broke into fintech by framing her experience this way: "I owned the merchant payout system that processed $400M in weekly settlements. I dealt with bank reconciliation delays, regulatory compliance for multi-state payroll, and a fraud ring that cost us $2M in Q3. I had to build real-time anomaly detection while maintaining 99.9% payout reliability." That's not fintech experience. But it's fintech-adjacent experience translated correctly.

The translation framework: identify 2-3 metrics in your current role that have a direct fintech equivalent. Approval rates = order completion rates. Fraud loss = return rate. Compliance = terms of service enforcement. Regulatory pressure = legal review cycles. Every domain has a fintech parallel if you look for operational complexity, not product similarity.

What Do Fintech PM Interviews Actually Test

Fintech PM interviews test three things: domain judgment, operational ownership, and regulatory awareness. Not product sense, not leadership principles, not "tell me about a time you disagreed with an engineer."

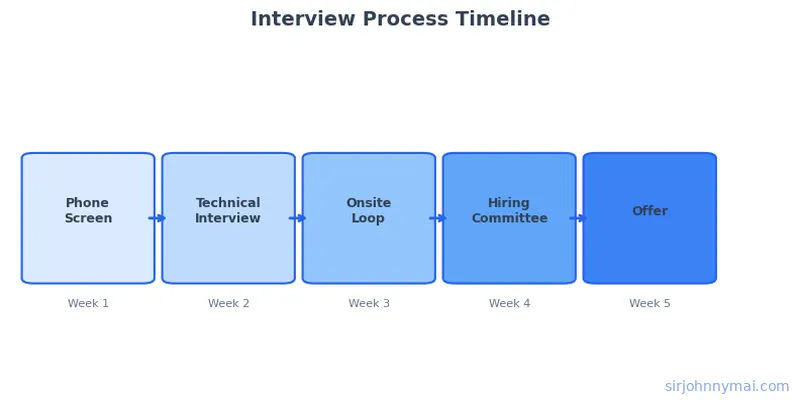

The interview process at most fintechs follows a specific structure: recruiter screen (15-30 minutes), hiring manager deep-dive (45-60 minutes), technical PM case study (60-90 minutes), cross-functional panel (3-4 sessions, 45 minutes each), and executive round (30-45 minutes). That's 5-7 rounds over 2-3 weeks. Some companies (notably Stripe and Block) add an additional technical assessment or written case.

The case study is where candidates fail most often. Not because the problems are hard, but because they're specific.

A typical fintech PM case study: "Our daily active user count is stable, but transaction volume per user has dropped 15% over two quarters. We suspect it's due to a new competitor offering lower fees.

What do you investigate first, and what's your recommendation?" The candidate who immediately jumps to competitive analysis misses the point. The strong answer starts with: "Before analyzing competitors, I need to understand whether this is a product issue or a segment issue. Let me look at cohort retention by signup source, transaction type distribution, and whether the decline is concentrated in high-volume users or across the board."

Not analysis, but prioritization under uncertainty. That's what fintech case studies test.

Smart Preparation Strategy

- Map your current experience to fintech metrics. Identify 3-5 operational metrics you own that have direct parallels to fintech KPIs (approval rates, fraud loss, processing latency, unit economics). Practice articulating these in fintech-native language.

- Study the regulatory landscape for the company's specific segment. If they're in lending, understand TILA and ECOA. If they're in payments, know PCI-DSS and AML basics. You don't need to be an expert, but you need to signal awareness that regulation shapes product decisions.

- Prepare 3-5 operational stories that demonstrate ownership under constraints. The strongest fintech PM candidates have stories about shipping product under regulatory deadlines, making trade-offs between growth and risk, or handling incidents that impacted company metrics directly.

- Practice case studies with a structured framework. The PM Interview Playbook covers fintech-specific case structures with real examples from Stripe, Block, and Brex interview processes—focus on how to structure a response when you don't have complete information, because that's the actual test.

- Research the company's regulatory history. Read their SEC filings, consent orders, or press releases about compliance initiatives. Interviewers notice when candidates can reference specific regulatory challenges the company has faced.

- Prepare thoughtful questions about the company's risk posture. Not generic questions about strategy—specific questions about how the company balances growth with regulatory compliance, how they've handled enforcement actions, or what keeps the CEO up at night. These signals cultural fit.

- Negotiate compensation structure, not just base salary. Understand the equity vesting schedule, the variable component targets, and the company's funding stage. Late-stage fintechs often have more predictable (but lower) equity upside than early-stage.

Common Pitfalls in This Process

Mistake 1: Studying technology instead of operations.

BAD: Spending weeks learning how blockchain works, what smart contracts do, or the technical architecture of payment rails.

GOOD: Understanding the operational challenges of running a payments business—reconciliation, settlement delays, bank partnership complexity, fraud attack patterns.

Mistake 2: Generic product sense answers.

BAD: "I would talk to users, run A/B tests, and prioritize based on impact."

GOOD: "I would first check whether the transaction decline is concentrated in a specific user segment or uniform across the base, because the root cause changes our response entirely."

Mistake 3: Treating fintech like any other product domain.

BAD: Focusing answers on user experience, retention loops, and growth experiments.

GOOD: Leading with regulatory constraints, risk trade-offs, and operational metrics that directly impact the company's ability to operate.

FAQ

Is fintech PM harder than other product roles?

Yes, but not for the reasons candidates expect. The difficulty isn't the product complexity—it's the operational burden. You will spend significant time on compliance reviews, legal meetings, and risk assessments that have nothing to do with building great product experiences. If you want to spend 100% of your time on user-facing product, fintech isn't the right fit.

Do I need financial services experience to get hired?

No, but you need to demonstrate operational complexity in your current role. The hiring signal is: can this person make decisions under regulatory pressure, own metrics that affect company survival, and navigate constraints that don't exist in other industries? You can signal this from any domain if you frame your experience correctly.

What's the career outlook for fintech PMs in 2025?

Strong, with caveats. The sector continues to grow, and fintech companies are still hiring PMs at higher rates than most tech verticals. But the market has normalized from the 2021-2022 boom. Competition for roles at category leaders (Stripe, Block, Ramp, Brex) is intense. The opportunity is in Series B-C companies where you can move faster and own more, but the failure risk is higher.

Ready to build a real interview prep system?

Get the full PM Interview Prep System →

The book is also available on Amazon Kindle.